Research

The fundamentals of Base

This research piece has been written by Michael Nadeau from The DeFi Report, in collaboration with Token Terminal.

1. The problem

At a high level, blockchain developers are primarily looking for two things:

- Scalable, easy-to-build on infrastructure.

- Access to millions of users (distribution).

As noted in our Arbitrum memo, blockchains sell block space (ledger entries). However, block space is a limited resource. Therefore, when user demand increases, the market instantly reprices a blockchain’s scarce resource. This prices out the typical user — making it impossible for developers to build apps that the average person can freely use.

Furthermore, crypto doesn’t have an “app store” just yet that can serve as a distribution platform for developers. Ethereum has broadly played that role to date.

2. The solution

On August 9th, Coinbase launched Base to the public — a secure and scalable L2 leveraging the OP (Optimism) stack. If you’re a developer, you get to choose where to build your app. With Base now in the mix, devs have a secure and scalable L2 on Ethereum with the following features:

- Distribution via access to Coinbase’s 110 million verified users.

- Access to 108 million Ethereum users (non-zero wallet addresses).

- Alignment with Optimism and a familiar tech stack (solidity & vyper programming languages).

- Opportunity to leverage Coinbase’s trusted brand as the only publicly traded crypto exchange.

- Interoperability with Ethereum and the largest network of developers and developer tooling in crypto.

- Shared security from Ethereum.

- Access to Coinbase’s vast network of investors, builders, and service providers.

- Frictionless user onboarding experience from fiat —> crypto —> onchain.

If you’re a developer, what’s not to like about this? When we scan the landscape of L2s today, we find it hard to find an alternative that can compete with that package.

Of course, other networks have money to throw at developers. As a publicly traded company, Coinbase can’t do that. And Base doesn’t have a token — which puts it at a disadvantage to competitors that can leverage their token as an incentive to bootstrap developer activity.

For example, Polygon just launched an $85m grant program via it’s native token, Matic — designed to draw builders to its ecosystem.

3. Who’s building on Base?

Remember, Base is only about 3.5 months old. But it’s growing fast.

A quick view of the projects driving the most gas fees over the last 90 days:

Pivoting to 90-day active users:

Finally, let’s look at the top projects by transactions:

Consumer apps

You’ll notice that a DeFi project isn’t leading within any metric we’ve covered. Rather, Base’s early success has been primarily driven by consumer use cases.

Friend.tech — a new social media app enabling creators to monetize their following with exclusive offers and content — has seen the most widespread use to date. With that said, we’d like to highlight a few apps that are not included in the top 10:

Blackbird is a restaurant app and loyalty program that is attempting to connect restaurants to their customers via Base’s crypto infrastructure. Through Blackbird, customers tap their phone on a near field communication reader (NFC - the device that allows smartphones to connect to payment readers) and create a membership token via NFTs. All customer engagement with the restaurant is then tracked (and eligible for rewards) onchain when a user “taps into” the restaurant.

It’s also noteworthy that Blackbird's CEO is Ben Leventhal, a co-founder of the dining network, Resy. The team recently raised $24m in funding led by a16z and has signed on about 80 restaurants to date.

Basepaint is a collaborative pixel art app on which artists meet daily to paint on a shared pixel-art canvas. The next day, the canvas is turned into a 24-hour open edition NFT mint. Once the mint concludes, that days artists receive a share of ETH from the mint. To date, artists have earned 160 ETH on the platform (approx. $320k). The project has 140k transactions over the last 90-days, placing it just outside the top 10 projects on Base.

4. How Base fits into Coinbase’s long-term vision

“We believe cryptocurrency is the future of money, and that building an equitable, accessible, and trusted open financial system will increase economic freedom around the world." - Coinbase’s mission statement.

When you consider that Coinbase is a centralized exchange that takes custody of user assets, the mission statement has at times seemed at odds with the reality of the business.

However, the launch of Base within the public Ethereum network lends credibility to Coinbase’s ultimate mission. It appears that the centralized exchange is simply the first necessary step toward achieving the ultimate vision of a more decentralized, open financial system.

Furthermore, with the launch of Base, we think Coinbase is making a move toward owning the infrastructure upon which the future rails of finance and consumer apps run. In some ways, they’re disrupting themselves to get there — by essentially pushing users onchain to DeFi — where trading fees are significantly lower than the average 1.3% retail traders are paying today. And where users custody assets themselves — leaving the Coinbase platform in the process.

So why does this make sense for Coinbase? From our perspective, there are 7 primary factors:

- Coinbase will earn a small fee for every transaction running through Base.

- Coinbase can build the “web3 app store” on Base (infrastructure with a small take rate).

- Coinbase could build tooling on Base to support the build-out of DeFi and the tokenization of real-world assets (products owned by Coinbase, supported by their prime brokerage wing). Remember, Coinbase already has a relationship with Blackrock, the largest asset manager in the world.

- Coinbase could build infrastructure to support 3rd party applications launching businesses onchain (AWS model).

- Coinbase Ventures could focus on seeding the next wave of apps building on Base — driving more enterprise value to the company.

- Coinbase owns one of the most widely used wallets in crypto — which could serve as a data monetization opportunity similar to search in web2. For example, Coinbase could leverage its distribution and earn “referral fees” for pushing users from the exchange to preferred partners in DeFi and other consumer apps building on Base.

- From a PR perspective, Base has aligned with Ethereum — a mission-driven ecosystem building the future of the internet in a more open, decentralized manner. Crypto natives support the move — so long as Coinbase doesn’t become a centralization concern.

5. Is Coinbase the Amazon of web3?

We see a lot of parallels between the maturation of Amazon over the years and where we think Coinbase may be heading.

Amazon launched in 1994 as an online bookstore. By 1998 they had aggressively expanded beyond books — to music, DVDs, movies, home improvement products, etc. By 2000 they had opened their own marketplace — enabling third-party orders.

But they never stopped innovating. Kindle. Amazon Prime. Streaming services. Original content. The products and services never stop. Along the way, Amazon realized they could offer web2 infrastructure services to others. They could take their learnings as a first mover, and help others build internet native products and services.

12 years after launching the online book store, AWS was born — a cloud computing platform serving as infrastructure for web2 app developers, enterprises, and governments. AWS does about $90 billion in revenue today — representing about 16% of top-line revenue for Amazon.

We think Coinbase’s growth arc could take a similar shape as Amazon’s.

Coinbase launched as a Bitcoin-only exchange in 2012. The second asset listing didn’t hit the exchange until 2015 when Ethereum launched.

Since that time we’ve seen a frenzy of activity within web3 — with Coinbase sitting at the epicenter of it all. Up until Coinbase’s IPO, retail trading fees dominated the business model — making up 96% of top-line revenue in Q2-21.

Since that time, we’ve seen significant diversification of Coinbase’s revenue lines. Today, Coinbase’s top-line revenue from trading is just 42%. Impressive diversification over the last 2 years. Here’s what they’ve added:

- USDC stablecoin: $172m in revenue in Q3 (via partnership with Circle)

- Staking: $74.5m in revenue Q3 (second largest liquid staking solution for ETH)

- Prime brokerage & custody: $15.8m in Q3 (partnership with Blackrock)

- Institutional derivatives platform: Launched in Q3, potentially a cash cow business replacing FTX & Binance (crypto derivatives are a $3 trillion annual volume business today).

- Venture portfolio: Coinbase is deeply tied in with the crypto VC space (their co-founder started Paradigm, a leading web3 venture firm) and has an ownership stake with many important infrastructure companies such as Alchemy.

Similar to Amazon, we think that Coinbase is well-positioned to leverage its intel as a builder in the space with its broad distribution (108 million verified users).

In doing so, Coinbase becomes an infrastructure company that builds products and tooling serving the future rails of finance and consumer apps. In essence, they could build the infrastructure for the merger of TradFi with crypto.

Finally, we think Coinbase will be looking to seed 3rd parties to build on Base. In doing so, Base becomes the infrastructure for the “web3 app store.”

We’ll see how it goes. Execution is everything. But we think this is the potential direction for the company in the coming years.

6. Base: financials & comps

Note that Base was launched to the public on 8/9/23 — therefore, our comps are on a 90-day basis. A quick rundown as to how Base is stacking up against its main competition:

- Revenue: Base comes in at #3 with Arbitrum outpacing them by 28%, and Optimism by 3.5%.

- Margin: Base currently has the lowest take rate across its competition. We’re keeping an eye on this to see if the margins improve moving forward — in line with the premium that Coinbase charges for staking (25%) and trading fees (1.3%). *Note that Base pays 15% of it’s top-line revenue to Optimism for leveraging the OP stack.

- Daily active users: Base comes in second to last here, outpacing only Avalanche. That said, 75k daily active users is impressive given the L2 launched just 3+ months ago.

- Avg. transactions/day: 623k/day puts Base at #4 — outpacing both Optimism and Arbitrum in this category. For reference, Ethereum does about 1.1m transactions per day.

- TVL: Base comes in last here with just $290m — not surprising given the most prominent projects on the L2 are consumer apps so far rather than DeFi protocols. With that said, Coinbase has over $130 billion in assets on the platform. This could potentially serve as rocket fuel for TVL growth on Base — assuming Coinbase can create the proper incentives and partnerships to drive assets onchain.

- Core devs: 22 core devs put Base in last place, but a respectable number nonetheless given the nascency of the project.

- Transactions/second: 7.21 transactions/second on average puts Base at #3 amongst its peers and more than Arbitrum, Optimism, and Avalanche. Solana is the clear outlier in this category.

- Cost/transaction: Base comes in at #4 — cheaper than Arbitrum and Optimism.

In summary, Base is clearly holding its own against the competition in its first 3+ months — an indication of the powerful role that Coinbase has played in its initial bootstrapping phase.

7. Base: competitive advantages

We think Base has six primary advantages over its competition:

1. Coinbase is part of crypto’s “cool club.” You won’t hear this discussed often, but it’s important. It really boils down to investor networks. The most prominent VC firms have vast networks of industry experts, institutional knowledge, and access to the best engineering talent. Coinbase (and Base via extension) is well connected amongst VC firms such as a16z, Paradigm, Union Square Ventures, etc. For example, friend.tech (the most successful app on Base to date) is a Paradigm portfolio company. Paradigm’s founder is the co-founder of Coinbase.

2. Distribution. Base has a unique advantage over other L2 networks in that Coinbase could incentivize users from the exchange to go “onchain” via the exchange. Furthermore, the Coinbase wallet could provide a massive data monetization opportunity via “referral fees.”

3. Fiat to crypto user onboarding. Coinbase solves this as the first step when onboarding a user. From there, the experience of moving onchain is significantly more straightforward than with other L2s.

4. Institutional knowledge. Coinbase is one of the OGs in the space, having started the exchange in 2012. We think the learnings over the last 11 years will be instrumental to Base’s success.

5. Security/brand. Coinbase is one of the most trusted companies in crypto. Given the number of smart contract hacks we’ve seen in the space, it’s possible that developers and users will put a premium on Base over other L2s.

6. Operational leverage. Given Coinbase’s institutional knowledge and engineering talent, we think it’s possible that a relatively small team of engineers could build a platform that ultimately ends up generating massive returns. Since its public launch, Base has averaged over $95k/day in revenue with a small team working on the project. What does this look like in a few years? Remember, this is an open-source project where Base (and Coinbase) will benefit from others building on the protocol.

The disadvantage?

Because Coinbase is a publicly traded company, it moves slower than your typical crypto start-up. They need to be more wary of getting into the crosshairs of regulators. For this reason, Base does not have a token. This could make it more difficult for the L2 to attract early users — since they cannot incentivize usage of the L2 with token airdrops.

8. Base: product offering

Today, Base is an onchain extension of Coinbase — serving as a general-purpose L2 for hosting 3rd party applications.

Where do we go from here? We think that there will be hundreds if not thousands of L2s in the future — serving specific use cases as “app chains” as well as “private L2s” connected to the public Ethereum network.

Given Coinbase’s partnership with Blackrock, it’s possible that Base becomes the infrastructure upon which Wall Street starts to build on crypto rails — launching “app chains” within Base to do so. For example, one could imagine Blackrock launching an L2 within Base for the exchange of tokenized private assets — a massive opportunity comprising hundreds of trillions of dollars in assets globally.

Of course, Base will likely host Coinbase’s centralized business units as well as a host of projects seeded by Coinbase Ventures.

Just as Arbitrum has introduced the ability for devs to build “app chains” via the Orbit and AnyTrust protocol, we’ll be looking for similar upgrades from Base in the coming months and years.

9. Base: business model

It’s important to note that Base is not a stand-alone L2. Rather, the team built it leveraging the OP (Optimism) stack. As part of their agreement, Base pays the greater of 2.5% of top line revenue or 15% of net profits.

In return, Optimism granted Base 2.75% of its tokens ($192m at current market prices).

In addition to paying 15% of its revenue to Optimism ($158k over the last 90 days), Base pays “call data” fees to Ethereum — just as Arbitrum and Optimism do.

The additional 15% fee puts Base at a slight disadvantage when compared to Arbitrum — which only pays Ethereum. That said, Base’s alignment with Optimism (and the 2.75% token allocation) is a nice offset.

Impact to Ethereum & Optimism

If Base wins, does Ethereum win? Does Optimism win?

Where does the most value accrue?

That’s the million-dollar question. In summary, we think all three will win together. What’s unclear at this stage is whether Optimism (or Arbitrum/another L2) wins as the general purpose L2 — with a vast network of “app chains” driving value to the L2 + Ethereum. Or whether Base serves that role as the “general purpose L2” while ultimately controlling the infrastructure for the “web3 app store.”

We think Ethereum ultimately wins as the “settlement layer” of web3 if the L2s are successful in scaling the network to a billion+ users.

10. Team

Jesse Pollak is the creator of Base and is the Head of Protocols at Coinbase. Prior to Base, Jesse led all of Coinbase’s consumer-facing engineering from early 2017 to mid-2021, including work on Coinbase, Coinbase Pro, and Coinbase Wallet. Jesse joined Coinbase through the acquisition of Clef, a company he founded and ran for five years that built passwordless identity solutions for crypto companies.

As mentioned, Coinbase is a crypto OG and very well networked within crypto. I can’t think of any other company in the industry that is in a better position to hire the most talented team of engineers, marketers, etc.

Social Presence (Twitter followers)

11. Conclusion

You may have to squint a little bit to see it, but we think Coinbase is positioning itself to be the most important infrastructure company in web3. As crypto merges with TradFi and web2 merges with web3 in the coming years, we expect Coinbase (and Base) to be right at the center of the all — playing a significant role in the next iteration of the internet.

The authors of this content, or members, affiliates, or stakeholders of Token Terminal may be participating or are invested in protocols or tokens mentioned herein. The foregoing statement acts as a disclosure of potential conflicts of interest and is not a recommendation to purchase or invest in any token or participate in any protocol. Token Terminal does not recommend any particular course of action in relation to any token or protocol. The content herein is meant purely for educational and informational purposes only, and should not be relied upon as financial, investment, legal, tax or any other professional or other advice. None of the content and information herein is presented to induce or to attempt to induce any reader or other person to buy, sell or hold any token or participate in any protocol or enter into, or offer to enter into, any agreement for or with a view to buying or selling any token or participating in any protocol. Statements made herein (including statements of opinion, if any) are wholly generic and not tailored to take into account the personal needs and unique circumstances of any reader or any other person. Readers are strongly urged to exercise caution and have regard to their own personal needs and circumstances before making any decision to buy or sell any token or participate in any protocol. Observations and views expressed herein may be changed by Token Terminal at any time without notice. Token Terminal accepts no liability whatsoever for any losses or liabilities arising from the use of or reliance on any of this content.

Stay in the loop

Join our mailing list to get the latest insights!

Continue reading

- Customer stories: Token Terminal’s Data Partnership with Linea

Customer stories: Token Terminal’s Data Partnership with Linea

Through its partnership with Token Terminal, Linea turns transparency into a competitive advantage and continues to build trust with its growing community.

- Introducing Tokenized Assets

Introducing Tokenized Assets

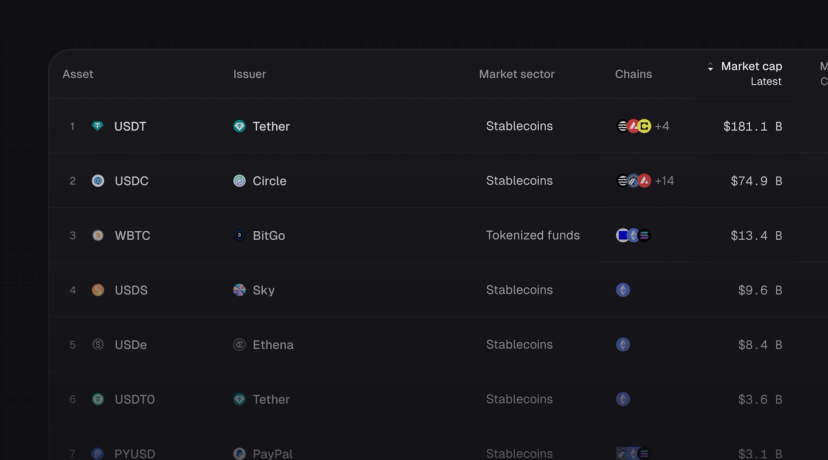

Token Terminal is expanding its standardized onchain analytics to cover the rapidly growing category of tokenized real-world assets (RWAs) – starting with stablecoins, tokenized funds, and tokenized stocks.

- Customer stories: Token Terminal’s Data Partnership with EigenCloud

Customer stories: Token Terminal’s Data Partnership with EigenCloud

Through its partnership with Token Terminal, EigenCloud turns transparency into a competitive advantage and continues to build trust with its growing community.